A Norfolk MP in a National Panic

The South Sea Bubble was not just a bad investment craze. It was a political and financial scandal built around the government’s need to manage debt after years of expensive war. It drew in ministers, courtiers, company directors, wealthy speculators, and ordinary investors who believed they had found a path to easy profit. When it collapsed in 1720, it damaged fortunes, reputations, and public trust.

Robert Walpole did not create the South Sea scheme. He was not the innocent outsider of later legend either. He invested in South Sea stock himself, and he moved in a political world where public office, private interest, and parliamentary management were closely tangled. Yet his importance is plain. When the scheme failed, Walpole became the man best able to contain the damage. The crisis helped make him the dominant British politician of the early eighteenth century.

Walpole also gives the story its Norfolk connection. Born at Houghton Hall in 1676, he entered Parliament for Castle Rising in 1701 and became MP for King’s Lynn in 1702. With a short interruption in 1712, he held the Lynn seat until 1742. King’s Lynn was not the centre of the Bubble. That lay in London, Westminster, the Treasury, and the financial markets. But Lynn was the parliamentary base from which a Norfolk landowner helped steer Britain through one of its most dangerous political scandals.

The Government’s Problem: Too Much War Debt

The scheme began with a real problem. Britain had borrowed heavily during years of war. Governments did not usually pay all wartime costs from taxes as they arose. They borrowed money and promised to pay lenders an income in future.

One way of doing this was through an annuity. An annuity was a promise to pay a fixed sum each year. For the lender, it was a steady income. For the government, it was an annual burden. The state had to keep making payments to thousands of creditors, often under terms that were difficult to change.

By 1720, ministers wanted to reorganise part of this debt. That was not foolish in itself. A better-managed debt might reduce the government’s yearly costs and strengthen public credit. The danger lay in the method chosen: allowing the South Sea Company to turn much of this government debt into company stock.

What the South Sea Company Promised

The South Sea Company had been founded in 1711. Its name suggested trade with the Spanish American world, then often described as the “South Seas”. The phrase was useful. It evoked silver, colonial markets, Atlantic commerce, and profits waiting to be claimed.

The reality was narrower and darker. The company’s best-known trading privilege was connected with the Asiento, the contract to supply enslaved Africans to Spanish America. After the Treaty of Utrecht in 1713, Britain gained rights in this trade, and the South Sea Company acquired the contract from the government. The company’s commercial image was therefore tied not only to imperial hope, but also to the Atlantic slave trade.

Even this grim trade did not produce the vast profits imagined by investors. Spain did not open its empire to free British commerce. The company had limited rights, not unlimited access to American wealth. By 1720, its great attraction was no longer what its ships might earn overseas. It was what its stock might do in London.

The Scheme, Put Simply

The South Sea scheme can be understood in stages.

The government owed money to many creditors. Those creditors held promises of future payment, including annuities. The South Sea Company offered to take over a large part of this debt. Creditors would give up their government annuities or other securities and receive South Sea stock instead.

Stock meant a share in the company. If the company prospered, stockholders might receive dividends. If other people wanted the stock, its price might rise, and holders could sell at a profit.

That was the temptation. A creditor with a dull but reliable government payment was invited to exchange it for stock in a company whose price was climbing. The company, meanwhile, would receive regular payments from the government and would become a vast manager of public debt.

The scheme looked clever because it seemed to offer something to everyone. The government hoped to make the debt easier and cheaper to manage. Creditors hoped to turn fixed income into larger gains. The South Sea Company hoped to grow enormously. Speculators hoped to buy stock and sell it for more. Ministers and insiders saw opportunities of their own.

But the arrangement depended on confidence. The company’s trading profits could not justify the enormous rise in its share price. Much of the excitement rested on the belief that someone else would later buy the stock at a higher price.

That is the heart of the Bubble. The price rose because people believed it would rise further. The rise itself became the advertisement.

See Appendix for an explanation of financial terms.

Why People Were Drawn In

The South Sea scheme did not look absurd to many people at the time. It had official weight behind it. Parliament approved it. Ministers supported it. The company had a royal charter and a formal connection with government finance. To an investor, this made South Sea stock look very different from a small private gamble.

The company also had the language of empire on its side. Spanish America sounded rich. The company’s name did a great deal of work. It allowed promoters and investors to imagine trading profits far beyond anything the company was likely to secure.

There was another lure. Buyers did not always have to pay the full price of stock at once. Shares could be bought through staged payments. That made speculation easier. A person could commit to buying stock, pay only part of the price immediately, and hope to sell at a profit before the later payments became troublesome.

This widened the market and sharpened the danger. People could take larger positions than they could comfortably afford. When prices were rising, that looked like opportunity. When prices fell, it became ruin.

Corruption at the Centre

The South Sea Company needed political approval, and it knew how to obtain it. The scheme passed through Parliament, but not in a clean atmosphere of disinterested public judgement. Company officers cultivated politicians and courtiers. Some leading figures were given favourable arrangements that allowed them to benefit from a rising stock price without taking ordinary risks.

John Aislabie, the Chancellor of the Exchequer, became one of the central figures in the scandal. Robert Knight, the company’s cashier, was later exposed as having arranged fictitious stock for important political figures, including Aislabie and the Earl of Sunderland. The higher the stock price rose, the more those arrangements could be worth.

This mattered because it corrupted judgement. Ministers were not merely deciding whether the scheme served the country. Some had private reasons to want the share price driven upward.

The Rise and Fall

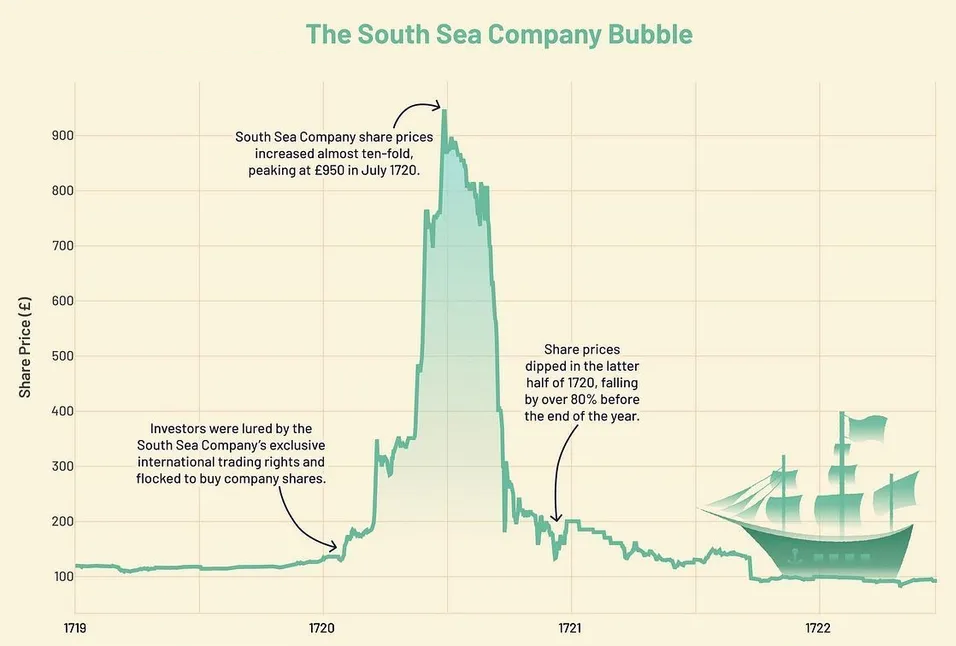

In 1720, South Sea stock climbed at extraordinary speed. Its price rose from a little over £100 at the beginning of the year to around £1,000 at its height in the summer. By October, it had fallen to about £150.

The speed of the rise helped create the crash. Early buyers seemed to be making fortunes. Their apparent success drew others in. The new buyers pushed the price higher still. The high price then seemed to prove that buying had been wise.

But the company had not become ten times more valuable in any real commercial sense. Its American trade could not support the price. Its financial scheme depended on continued belief. Once doubts spread, the same logic worked in reverse. People wanted to sell. Falling prices frightened others into selling. Those who had bought late were trapped.

The anger that followed was not only about lost money. It was about betrayal. Investors had been encouraged to believe in a scheme wrapped in public authority. Parliament, ministers, and the court all appeared tainted by the collapse.

Walpole’s Moment

Walpole’s great opportunity came after the damage had been done. The question was no longer whether the Bubble could be prevented. It had burst. The question was whether the crash would bring down the government, destroy public credit, and expose the Hanoverian regime to deeper danger.

The court itself was not untouched. George I’s German favourites, especially the Duchess of Kendal, were widely suspected of profiting from the scheme, and the Princess of Wales was also drawn into the world of South Sea stock. Walpole’s task was therefore not only to punish company directors and fallen ministers, but to prevent the scandal from reaching too far into the royal household. This was the origin of the hostile charge that he acted as a political “screen”, protecting the court while allowing lesser men to fall.

He had to manage several pressures at once. Investors demanded relief. The public wanted punishment. Parliament wanted inquiry. The court wanted protection. The Whig ministry wanted survival. The financial system needed calm.

Walpole’s answer was controlled damage limitation. He supported inquiry and allowed some punishment, but he also worked to stop the scandal from consuming the entire political order. Aislabie was expelled from the Commons in March 1721. South Sea directors were investigated, and some assets were confiscated. Yet not every powerful figure suffered equally. Walpole helped shield Sunderland from full censure, earning from critics the nickname “Screen-Master General”.

The criticism was not baseless. Walpole was not purifying politics. He was preserving government. His achievement was practical rather than moral. He gave the public enough punishment to show that the scandal had consequences, but not so much exposure that the regime itself was broken.

From Crisis to Power

The Bubble ruined some men and weakened others. Sunderland’s authority declined. Aislabie fell. The South Sea directors became convenient targets for public fury. Walpole emerged as the politician who could manage the Commons, speak the language of finance, and calm the court.

In April 1721, he became First Lord of the Treasury and Chancellor of the Exchequer. He remained in power until 1742. Later historians and official accounts often call him Britain’s first prime minister, though the title did not yet have its modern formal meaning.

The South Sea crisis therefore did not merely test Walpole. It helped define him. His power rested on finance, parliamentary management, royal confidence, and political patience. The Bubble showed why those skills mattered.

King’s Lynn and the Wider Story

Walpole’s King’s Lynn connection should be kept in proportion. The town was not a financial centre in the South Sea affair, nor was the Bubble a Lynn story in any direct local sense. Its machinery was metropolitan and parliamentary.

Even so, the connection is real. Walpole acted in the crisis as the MP for King’s Lynn. The borough formed part of the political foundation that allowed him to remain in the Commons for decades. In that sense, Lynn had a place in the making of the man who emerged from the South Sea wreckage as Britain’s chief minister.

What the Bubble Revealed

The South Sea Bubble exposed the workings of early Georgian power. It showed a state burdened by war debt. It showed how government borrowing had become a central matter of national politics. It showed how a chartered company could stand between the state and investors. It showed how imperial promises could be used to inflate financial hopes. It showed how the slave trade could sit inside respectable schemes of public finance. It showed how easily political influence and private profit could become entangled.

It also showed Walpole’s particular gift. He was not a visionary reformer in this crisis. He was a manager of consequences. He knew that a complete exposure of corruption might satisfy anger but endanger the regime. He chose containment.

That choice left a stain. Some of the guilty escaped lightly. Yet politically, it worked. Public credit steadied. The government survived. Walpole rose.

Conclusion: Not Walpole’s Scheme, But Walpole’s Crisis

The South Sea Bubble was a government-backed debt scheme inflated by speculation, political favour, imperial fantasy, and corruption. Its central trick was to persuade holders of government debt to exchange steady payments for South Sea stock, then to keep that stock rising long enough for the company, insiders, and speculators to profit.

The trick could not last. The company’s real earnings could not support the price. Once confidence failed, the market collapsed.

Walpole did not make the Bubble. But he made his career from its aftermath. As MP for King’s Lynn, he entered the crisis as a powerful Norfolk Whig and emerged as the indispensable manager of government. The Bubble broke fortunes and exposed corruption. It also helped make Robert Walpole the dominant political figure of Georgian Britain.

Appendix: Financial Terms Explained

| Term | Explanation |

|---|---|

| Annuity | A promise to pay a fixed sum each year. In this context, the government owed annual payments to people who had lent it money. |

| Bubble | A situation in which an asset’s price rises far above what its income or real prospects can support, usually because buyers expect to sell at a higher price later. |

| Company stock | Shares in a company. Owning stock meant owning a claim on the company’s profits or future payments. |

| Creditor | A person or institution owed money. Government creditors held promises of payment from the state. |

| Debt conversion | The process of changing one kind of debt into another. In 1720, many government creditors were encouraged to exchange government payments for South Sea stock. |

| Dividend | A payment made by a company to its stockholders. Investors hoped South Sea stock would bring dividends, though rising prices became the greater attraction. |

| Fictitious stock | Stock entered on paper for favoured people without normal purchase and payment. It allowed insiders to profit from a rising price and was a form of bribery. |

| Instalment payment | A system in which buyers paid for stock in stages rather than all at once. This made speculation easier and more dangerous. |

| Joint-stock company | A company owned by shareholders. The South Sea Company was a chartered joint-stock company. |

| National Debt | Money owed by the government to lenders. It grew heavily because of war. |

| Public credit | Trust in the government’s ability and willingness to pay its debts. If public credit failed, borrowing became harder and more expensive. |

| Royal charter | A formal grant from the Crown giving a company legal status and privileges. A charter made a company look more official and trustworthy. |

| Share | A unit of ownership in a company. In this period, “stock” was often used in a similar way. |

| Speculation | Buying an asset in the hope that its price will rise, rather than mainly for the income it produces. |

| Subscription | An agreement to buy stock, often with payment made in stages. South Sea subscriptions helped widen participation in the Bubble. |

© James Rye 2026

Book a Guided Tour with a Trained and Qualified King’s Lynn Guide Through Historic Lynn

References

Britannica, Encyclopaedia. “Robert Walpole, 1st Earl of Orford.” Written by J. H. Plumb. Encyclopaedia Britannica. https://www.britannica.com/biography/Robert-Walpole-1st-Earl-of-Orford

Carswell, John. The South Sea Bubble. Revised ed. Stroud: Sutton, 1993.

Dickson, P. G. M. The Financial Revolution in England: A Study in the Development of Public Credit, 1688–1756. London: Macmillan, 1967.

GOV.UK. “Sir Robert Walpole.” Past Prime Ministers. https://www.gov.uk/government/history/past-prime-ministers/robert-walpole

History of Government Blog. “Sir Robert Walpole, Whig, 1721–1742.” Published 20 November 2014. https://history.blog.gov.uk/2014/11/20/sir-robert-walpole-whig-1721-1742/

History of Parliament Trust. Littleton, Charles. “A Trojan Horse in the House of Lords? The South Sea Company and the Peerage.” Published 9 January 2020. https://historyofparliament.com/2020/01/09/south-sea-company-and-peerage/

Hoppit, Julian. “The Myths of the South Sea Bubble.” Transactions of the Royal Historical Society, 6th ser., 12 (2002): 141–165.

Kleer, Richard. “‘The Folly of Particulars’: The Political Economy of the South Sea Bubble.” Financial History Review19, no. 2 (2012): 175–197.

Paul, Helen J. The South Sea Bubble: An Economic History of Its Origins and Consequences. London: Routledge, 2011.

Quinn, William. “The South Sea Bubble 300 Years On.” Economic History Society, 8 June 2020. https://ehs.org.uk/the-south-sea-bubble-300-years-on/

Royal Museums Greenwich. “What Was the South Sea Bubble?” https://www.rmg.co.uk/stories/maritime-history/south-sea-bubble